By Miguel Salomon, P.E., Sandcastle Homes

The year 2022 has been a whiplash for the real estate market. We started with a frenzied market. Interest rates were low (3.45 percent, per Freddie Mac). There were more buyers than available homes. By a lot! Buyers would view a new listing and, before they could act, it was SOLD! As a result, an extraordinary share of transactions involved bidding wars among multiple buyers, and homes were selling above asking price.

Then, life happened. Inflation numbers came in at the highest rate in decades, over 8 percent. The Fed started hiking interest rates aggressively. By May, mortgage rates were over 5 percent. Still good by historical terms but high by recent memory. And with no sign of letting up. Today, the rate for a 30-year, fixed rate mortgage is about 7 percent. Major sticker shock! Suddenly, that monthly payment on your client’s dream home was significantly higher than when they began their quest. And the reaction from the market was swift.

Advertisement

Buyers took a pause. The frenzy was over. And over the past few months, we saw inventory of available homes begin to rise.

We are still far from “equilibrium,” with inventory still extremely tight by historical standard. But the psychology has clearly shifted. Buyers can now afford to take their time without fear of missing out. And sellers are becoming more flexible on their pricing and terms.

Meanwhile, as more people pulled back from buying and decided to lease for another year, the rental market became increasingly tight. And rents have been sharply on the rise.

So, what does this all mean? Is it a good time to buy a house? Should potential buyers wait it out? I certainly have no crystal ball. But I am a numbers guy. So, let’s look at the economics.

The New Math

There has been a lot of press coverage around the rapid rise in mortgage rates and their impact on the housing market. But I have not seen a single article that attempted to look at the total cost of home ownership in comparison to, say, January 2022, when mortgage rates were 3.5 percent. So, I will summarize my analysis and some surprising revelations.

Everyone’s situation is different, and each buyer’s personal situation will certainly determine which decision is right for them. But let’s see what the numbers tell us, based on some typical cases.

Up until 2017, the U.S. tax code contained strong incentives to encourage home ownership. But the significant overhaul of the tax code that year took those incentives away for a huge percentage of homeowners. What happened? For starters, the standard deduction for a single person went up from $6,350 in 2017 to $12,000 in 2018. For married couples, filing jointly, the deduction went from $13,000 to $24,000 (and is indexed for inflation). In addition, the deductibility of state and local taxes, which includes property taxes, was capped at $10,000. So why does this matter?

Everyone is eligible for the standard deductions. But some people can get a better tax break by choosing to itemize deductions. Basically, if your itemized deductions are more than the standard deduction, you itemize. Otherwise, you take the standard deduction.

Historically, anyone with a mortgage would itemize. The mortgage interest plus property taxes were almost certain to exceed the standard deduction, even at 3 percent mortgage rates. But that all changed after 2017. Suddenly, homeowners found that they were better off taking the standard deduction. Or, if they did itemize, the benefit was marginal and not a major factor in their personal economics. The mortgage interest and property taxes that they were paying no longer offered any major advantage in terms of income tax savings!

And this is the piece that has received little or no attention in the press. The higher interest rates suddenly changed the economics! New homeowners can suddenly get a significant break on their income taxes again!

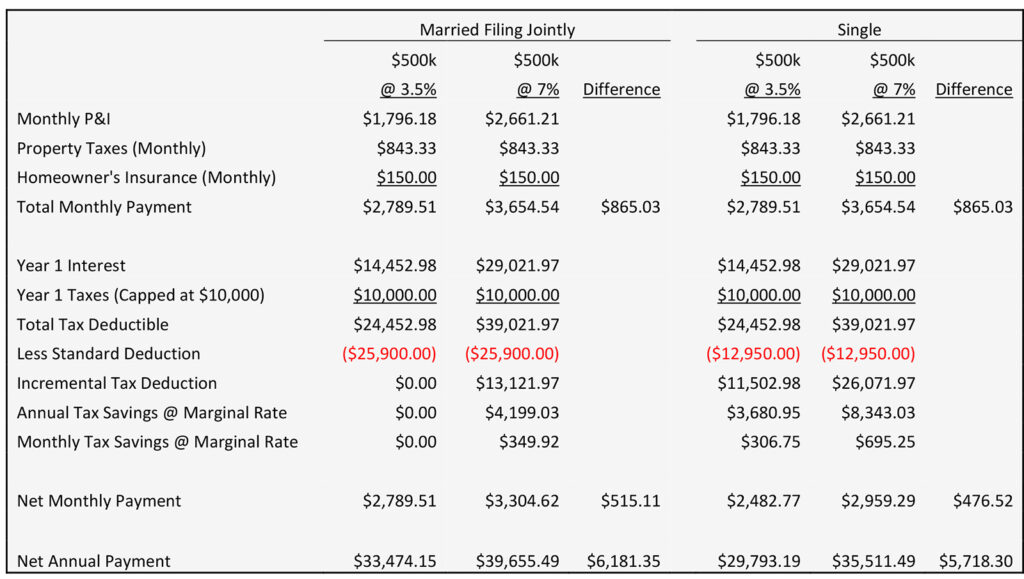

Below is a chart outlining the “new math.” Figure 1 below compares monthly payments at 3.5 percent versus 7 percent for a single person as well as for a married couple, filing jointly.

What we see above is that, while the higher interest rates have a significant impact on the monthly payment, the income tax savings offset about 40.5 percent of the increase for a married couple fling jointly and 44.9 percent for a single person. That’s huge!

And the married couple, who was previously unable to itemize deductions, may now be able to deduct additional, non-housing related items, such as healthcare expenses or certain charitable donations. But an extra $500/month is still significant.

Other Financial Factors

To truly compare the total cost now versus January 2022, we need to look at the whole picture. In January, in order to buy that home listed at $500,000, you likely had to offer above asking price. Conservatively, let’s assume that 3 percent above asking would get you the home. That’s an extra $15,000!

By contrast, it’s not crazy to think that, in the softer market, you might actually be able to get that same house for 97 percent of the asking price. Now the difference in price is double, or $30,000. That will cover the extra $500/month for 60 months, or five years!

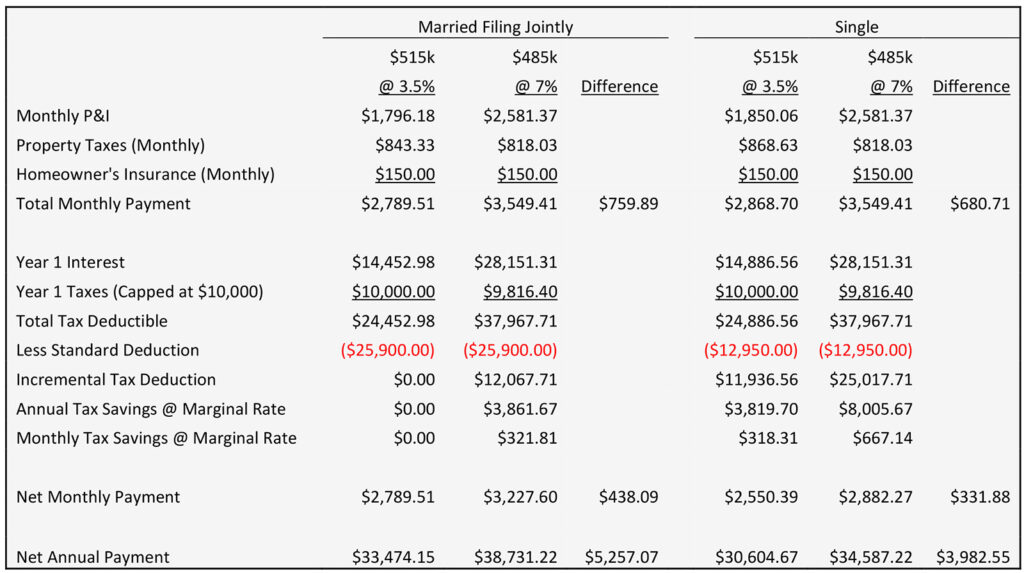

Let’s look at it another way. What happens to our chart if we compare financing a purchase at $515,000 at 3.5 percent with a purchase at $485,000 at 7 percent? The difference in monthly payments becomes $438 for the married couple and only $332 for the single person. (See chart below)

What About Renting?

Having bought my first home at age 23, I am convinced that home ownership is one of the pillars upon which we build our personal wealth. Paying rent is equivalent to flushing cash down the toilet (please don’t tell my tenants). Since 1891, the average home has appreciated by 3.2 percent annually and stayed ahead of inflation by an average of 0.3 percent. Paying rent has a guaranteed rate of return of negative 100 percent!

And while the net total payment for that $500,000 home has gone up by nearly $300 to $400 per month, rents have also been on the rise and have largely kept up. And 100 percent of that rent payment is gone forever, whereas approximately $340/month of your mortgage payment will go towards paying down the principal of your loan, building additional equity.

Take Away

So, what does it all mean? Here are my takeaways from all of this:

Nobody is happy about increased mortgage rates. But the net impact is not as bad as you might think.

If you already own a home, you don’t need to move and you are locked in at a low interest rate, it probably makes sense to stay put or, at least hold on to your existing home as a rental property.

If you are still renting, don’t! For the first time in years, you have plenty of homes to choose from and sellers are suddenly flexible on price and terms. And while interest rates are higher than they have been in 20 years, most economists expect that we will return to a low interest rate environment within two years, at which time you can refinance.

About the Author: Miguel (Mike) Salomon. P.E. is president, founder and co-owner of Sandcastle Homes, Inc. Miguel has a bachelor’s degree in Civil Engineering and an MBA with a concentration in Finance, both from the University of Texas at Austin. He is a licensed Texas Real Estate Broker and licensed Texas Professional Engineer.